Project Cost Management: Complete Guide 2026

Stay Budget-Savvy: Monitoring your project budget helps you avoid overspending, keep stakeholders happy, and keep the project on track for success.

Stakeholders Matter: Keep stakeholders informed about budget health to foster trust and satisfaction, which will increase your chances of project success.

Use Software Tools: Project management software tools help you automatically track budget and costs and alert you early when things are going off the rails, so you can adjust quickly.

Without a keen eye trained on your project budget and how quickly you’re burning through it, you’re liable to end up way over budget, which your stakeholders and clients won’t be happy about. You’re also risking total project failure.

Here’s how to do project cost management (with the help of project management software) so you can keep your project on track and flag any budget issues as early as possible. I’ll also share best practices and tools that can help you optimize your project costs.

What Is Project Cost Management?

Project cost management is the process of planning, estimating, and controlling costs so that your project can be completed within the approved budget. It starts in the project planning phase of project management and needs to be monitored throughout the project life cycle.

Why Is Cost Management Important?

Project cost management is important because it directly affects project profitability and viability, and it allows you to make sure financial resources are efficiently used. Its primary functions include planning, estimating, determining the budget, and controlling costs:

- Planning: As a project manager, you identify the financial resources necessary for the project and create a cost management plan that outlines how costs will be managed and controlled.

- Estimating costs: Set realistic budgets and evaluate variable and fixed costs associated with project activities.

- Budgeting: Establish your project budget for approval.

- Monitoring and controlling costs: Track expenses against the budget, analyze variances, and implement corrective actions when necessary.

Benefits of Effective Cost Management

Effective project cost management provides these three key benefits and contributes to the overall success of your projects.

- More profitability: Strong cost management helps you complete projects on time and within budget, which leads to higher profitability and helps you maximize your company’s return on investment (ROI).

- Increased stakeholder satisfaction: You’ll be able to maintain transparency and open communication about budgetary constraints and financial decisions to build trust with stakeholders. You’ll also better manage expectations and encourage collaboration among your team members.

- Improved productivity: When your project costs are accurately estimated and monitored, you can allocate resources more efficiently and make sure personnel, equipment, and materials are used optimally. This improves productivity, minimizes waste, and reduces unnecessary costs.

Key Challenges With Project Cost Management

Cost management can be impacted by these three challenges, which can complicate the successful execution of your projects.

1. Inaccurate cost estimation

Cost estimates are often based on historical data, but if conditions change or there’s a lack of reliable data, your estimates can be significantly off, which can lead to budget overruns and financial strain.

Inaccurate estimation can also result from inexperience or insufficient understanding of a project's scope. Get input on cost estimates from your team or other stakeholders early in the planning process. If you're working on construction projects, you might also use AI in construction estimating to help with this.

2. Unclear or changing stakeholder expectations

Outside stakeholders can have varying priorities and may not fully understand the complexities of the project budget, which can lead to conflicts and misunderstandings.

They might complicate your project by suggesting scope changes or other ideas without any understanding of their impact on the budget, which can mean unexpected costs if you don’t manage this properly. Communicate regularly with your stakeholders to make sure everyone is aligned on budgetary constraints and project goals.

Read more: Looking to better manage outside stakeholder expectations? Check out our list of the best client database software solutions.

3. External factors

External factors like economic fluctuations, regulatory changes, and market volatility can impact your projects. These types of situations are often unpredictable and can impact resource planning and cost control, project timelines, and the overall budget. Keep a close eye on external factors and adjust your cost management strategies accordingly.

How To Create A Cost Management Plan

Use these steps to create a cost management plan that aligns with your project goals and scope.

1. Review Scope & Deliverables

Review your project’s scope, deliverables, objectives, timelines, and outputs to make sure all aspects are clearly defined. Engage your stakeholders to gather input and get buy-in as well. This helps avoid scope creep that can lead to unplanned costs and delays.

Document this information in the cost management plan for everyone to reference throughout your project.

2. Determine The Required Resources

Identify all the resources you need to execute your project effectively. This includes human resources, materials, equipment, and any external services that may be required. This will provide a baseline for your cost estimation.

Involve your team members and subject matter experts during this process. Their insights into the specific project tasks and needs will help make sure you haven’t missed anything, and will promote engagement and commitment. You should also evaluate resource availability, as shortages or delays can increase expenses and project timelines.

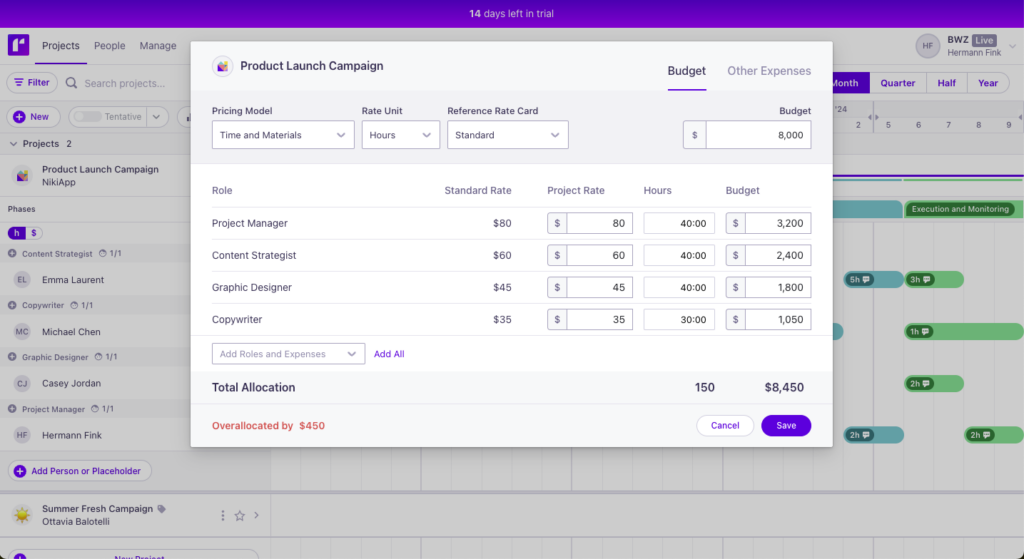

3. Estimate Costs

Assess all identified resources and their associated costs. Refer to your work breakdown structure (WBS) and use estimation techniques like analogous, parametric, and bottom-up estimating to derive realistic cost projections.

- Analogous estimating: Use similar past projects as a reference point when you’re developing estimates for the current project.

- Parametric estimating: Use statistical relationships between variables to calculate costs.

- Bottom-up estimating: Break down project tasks into smaller components and estimate costs for each.

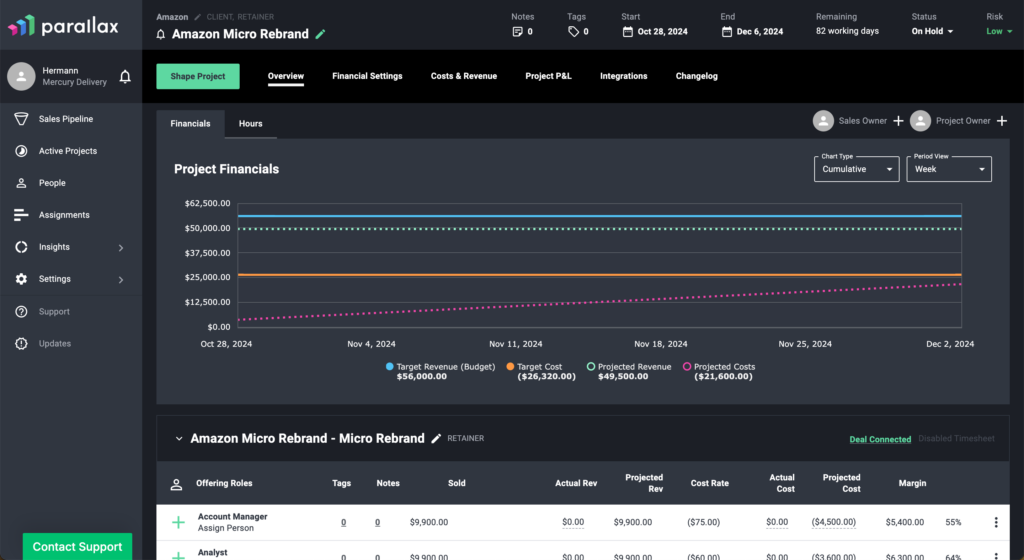

4. Monitor & Control Costs Throughout The Project

Keeping a close eye on costs throughout the project life cycle allows you to identify potential cost overruns early and implement corrective actions. This involves regularly tracking actual costs against your approved budget and analyzing cost variances.

For cost control, establish performance metrics and indicators that you’ll use to quantify project performance and identify areas that require attention. For example, earned value management (EVM) compares planned progress with actual cost performance in terms of cost and schedule. This metric tells you whether your project is on track, ahead, or behind schedule.

Tools For Managing Project Costs

Project management software and tools are your best bet for budgeting, forecasting, expense tracking, and reporting. If your project involves financial management, consider project management software that integrates with QuickBooks to streamline expense tracking, automate invoicing, and align budgets with your accounting system. These tools often offer customized dashboards and other features to help you:

- Create your project budgets

- Allocate resources

- Handle resource management

- Improve time tracking (either with a built-in tool or through an integration with time tracking software)

- Monitor expenses in real time

- Streamline your workflows

- Facilitate collaboration among team members

- Provide essential and timely insights into financial performance

- Update stakeholders on task and project progress

- Report financial discrepancies

- Deliver transparency

- Improve accountability

Here are the most popular project management software tools currently on the market:

Clicks on the links below may earn a commission, which supports our independent testing and review of software and services. Learn more about how we stay transparent.

You can find more options on our list of the best project cost management software.

Best Practices For Managing Project Costs

Here are some of my best practices for managing project costs and increasing profitability and client satisfaction.

- Anticipate surprises: To avoid surprises and prevent cost overruns, create a risk management plan and note risks that will directly impact the budget if they occur. Make a mitigation plan to address them.

- Remain realistic and practical: Adopt a zero based budgeting approach, where expenses must be justified for each new period rather than carrying forward previous budgets. Scrutinize every line item to make sure only necessary expenditures are approved.

- Set aside a contingency fund: This can provide a safety net for those unexpected costs.

- Practice continuous cost monitoring: Review financial performance against the budget and forecasts regularly.

Join For More Cost Management Insights

Want to connect with other digital project managers to share resources and best practices? Join our membership community and get access to 100+ templates, samples, and examples, and connect with 100s of other digital project managers in Slack.

{kind=link}